Barry Scheer

+31(0)88 253 1143 | bscheer@alfa.nl

![]()

26 februari 2021 | Door: Barry Scheer

If a foreign employee decides to work in the Netherlands, this employee may incur additional costs, the so-called extraterritorial costs. As an employer, you may give a free (tax exempt) compensation for the extraterritorial costs incurred by the employee. Instead of reimbursing the actual extraterritorial costs, an employer may also reimburse the extraterritorial costs by providing 30% of the salary, including reimbursement, tax exempt. This scheme is known as the 30%-ruling. Of course certain conditions have to be met.

The 30%-ruling applies if the employee has specific expertise that is not or scarcely available on the Dutch labour market. The employee has that specific expertise if the taxable salary in the Netherlands, excluding the 30%-allowance, is more than € 38.961 in 2021.

The employee is younger than 30 years old and has a master's degree

In case the employee is younger than 30 and has obtained a Dutch master's degree or an equivalent foreign degree at the university, the 30%-ruling applies if the taxable salary in the Netherlands, excluding the 30%-allowance, is more than € 29.616 in 2021.

The employee is involved in scientific research

Does the employee's work in the Netherlands consist of conducting scientific research at a designated research institution? In that case, the 30%-ruling always applies. The level of the employee's salary is not relevant for this.

Childcare leave does not affect the salary criteria of the 30%-ruling

Sometimes, by taking parental or maternity leave, an employee no longer meets the salary criteria of the 30%-ruling, as described above. In such case, a possible salary reduction as a result of taking these forms of leave will not be taken into account for the application of the salary criteria. The State Secretary for Finance has also approved (with retroactive effect from 1 July 2020) the salary reductions as a result of the following forms of leave will also be disregarded:

In addition to the specific expertise requirement, as described above, the employee must be regarded as an "incoming employee". This refers to the employee who comes to the Netherlands to work.

The 30%-ruling only applies to employees who lived more than 16 months at a distance of more than 150 kilometers from the Dutch border in the 24 months before their first working day in the Netherlands. As an employer, you can’t use the 30%-ruling for incoming employees from Belgium and Luxembourg. Employees from Northern France, large parts of Germany and a small part of the United Kingdom are also not eligible for this scheme.

Exceptions

Of course there are exceptions to this limitation. The restriction doesn’t apply to employees who come from the Dutch border region and who meet the following 3 conditions:

Exceptions to the main rule may also apply to PhD graduates.

The 30%-ruling has a maximum term of 5 years. The term of the 30%-ruling can be limited by periods of previous residence or work in the Netherlands in roughly 25 years before the date of arrival in the Netherlands.

During the term of the 30%-ruling, the income standard must be continuously reviewed to determine whether the employee still meets this standard. If the annual salary is, at a certain point, lower than the income standard, the 30%-ruling will be canceled retroactively to 1 January of that year. If the employment contract begins or ends in the course of a year, the salary may be re-calculated to an annual salary.

Employees who have obtained a Dutch master's degree or an equivalent foreign degree at the university, and to whom the reduced income standard applies (€ 29.616, excluding the 30%-allowance), must meet the higher standard from the month after the month in which they turn 30 (taxable annual salary of € 38.961, excluding the 30%-allowance). See also the "Specific expertise" section.

For an employee who transfers to a new employer during the term of the 30%-ruling, may continue the 30%-ruling under certain conditions. The new employer must submit a new request together with the employee. The new employment relationship must be entered into force within three months after the end of the old employment relationship.

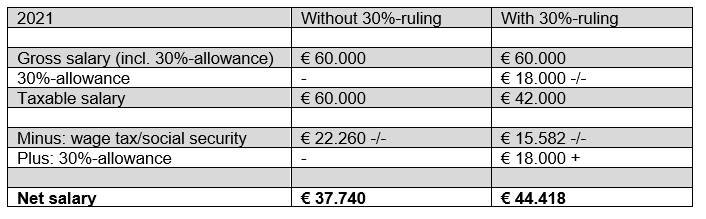

In this example, the 30%-ruling results in an annual net benefit for the employee of € 6.678.

Please do not hesitate to contact us in you want to know more about the 30%-ruling and if the 30%-ruling can apply for you or your employee.

Our tax specialists will advise and assist you in setting up your business in the Netherlands and will inform you on the taxation for your company and (incoming) employees in the Netherlands.

Read more