Matthijs van Dorssen

Director International

+31(0)88 253 3208 | mvandorssen@alfa.nl

![]()

19 oktober 2021 | Door: Matthijs van Dorssen

Most of the times the tax rates and credits are heavily changed in each Tax Plan. This year most rates will stay virtually identical.

A few trends are stated below:

All changes to rates are presented below.

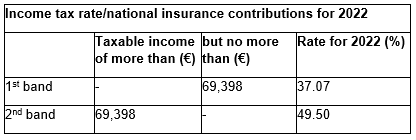

The rate applicable in the 1st band is being lowered slightly: from 37.10% to 37.07%. This band is also being widened to € 69,398 (€ 68,507 in 2021). The second tax band will remain unchanged.

Reduction of rates of relief in Box 1

Do you have an income higher than 69.398 euros? Important reliefs, like mortgage interest, are only deductible against a rate of 40 percent in 2022. Is jouw inkomen in box 1 in 2022 hoger dan 69.398 euro? The applicable rate in 2021 is 43 percent. The rate will be lowered until the rate of the first band of 37,07 percent in 2023.

Please note: the lowering of the applicable rate on reliefs is already final.

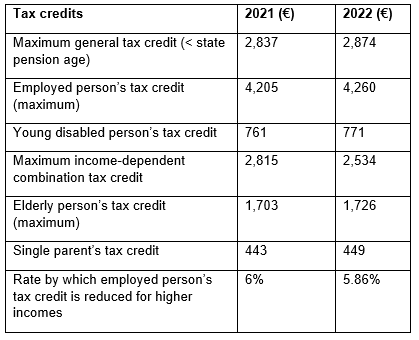

Everyone is entitled to a general tax credit – a credit against income tax. This credit is dependent on your income: the lower your income, the higher the credit. The general tax credit will be increased slightly in 2022. The rate by which the employed person’s tax credit is reduced for higher incomes is being lowered slightly from 6% to 5.86%.

The self-employed person’s allowance is an amount that entrepreneurs can deduct from their profit for income tax purposes, provided that they have worked as an entrepreneur for at least 1,225 hours in a calendar year. It reduces the amount on which you have to pay income tax. The self-employed person’s allowance is once again being reduced further. The maximum self-employed person’s allowance in 2022 will amount to € 6,310 (2021: € 6,670). This allowance will ultimately be cut to € 3,240 in 2036.

Please note: the reduction of this allowance is already final.

In 2022 the rate in Box 2 will remain the same as in 2021: 26.9%. The rate of 26.9% will apply to benefits from substantial shareholdings, such as dividends that are paid to a shareholder (director/major shareholder) and become part of his private assets, and capital gains on the sale of shares.

Please note: Are you considering making a dividend payment in 2021? If you have benefited from coronavirus support measures, pay close attention to the relevant regulations, as under some of these measures you are prohibited from distributing a dividend.

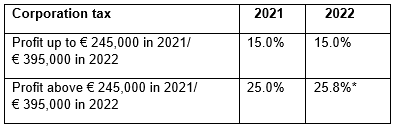

Corporation tax rates will remain unchanged. The widening of the band that was announced last year has been included in the Tax Plan. In 2022 the 25% rate will apply to profits above € 395,000.

* Preliminary

* Preliminary

The widening of the first band is already final.

Tip: If the expected profit of a tax entity for 2022 is well above € 395,000, you may obtain a tax advantage by terminating the tax entity. That is because you will then be able to benefit from the lower rate several times. Although the tax advantage appears simple to calculate, it may be outweighed by unforeseen drawbacks that result from terminating the tax entity. You should therefore check in good time whether this is an attractive option for you.

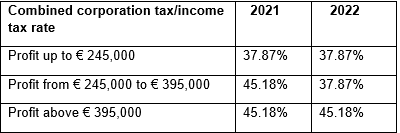

The combined corporation tax/income tax rate is as follows:

Director International

Read about the measurements for different subjects: