Matthijs van Dorssen

Director International

+31(0)88 253 3208 | mvandorssen@alfa.nl

![]()

28 september 2020 | Door: Matthijs van Dorssen

The high tax rate for the Corporate Income Tax will not be changed although this was announced earlier. The low tax rate will be lowered again and the profit applicable for the low tax rate will be increased. As a result the fiscal unity for the Corporate Income Taxes will be less favorable.

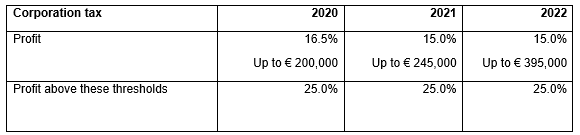

With effect from 1 January 2020 the lower rate of corporation tax was cut from 19% to 16.5%. The higher rate remained at 25%. These rates were due to be reduced further to 15% and 21.7% respectively with effect from 1 January 2021. However, it was recently decided that the higher rate will not be cut. This will therefore remain at 25%, although the lower rate will still be reduced to 15%.

Adjustments will also be made to the bands. In 2021 the 25% rate will only apply to profits in excess of € 245,000 and in 2022 to profits of more than € 395,000.

The corporation tax rates in 2021 and 2022 will be as follows:

The rate in box 2 is currently 26.25%. It had already been decided last year that this rate would increase to 26.9% with effect from 2021. There will be no changes to this plan. The rate of 26.9% will apply to benefits from substantial shareholdings, such as dividends that are paid by a private limited company to a shareholder (director/major shareholder) and become part of his private assets, and capital gains on the sale of shares.

Tip:

Due to the increase in the rate, it may be advantageous to distribute a dividend in 2020. Are you considering making a dividend payment in 2020? If you have benefited from coronavirus support measures, pay close attention to the relevant regulations, as under some of these measures you are prohibited from distributing a dividend.

At present, profits resulting from innovative activities are taxed at 7% for corporation tax purposes, subject to certain conditions. This rate is increasing to 9% in 2021. The innovation box was introduced as a tax incentive to encourage entrepreneurs to carry out innovative research. To be eligible for the innovation box, you need R&D declarations, which you can apply for at RVO.nl for research and development work.

At present, a loss can be carried back one year and carried forward six years. From 2022 the intention is to allow losses to be carried forward without any time limit. It will be possible to offset losses (carried forward and back) against up to € 1,000,000 of taxable profit. If the profit is higher, losses can only be offset against up to 50% of the profit above € 1,000,000 in any one year.

Please note:

A legislative proposal still has to be submitted.

At present, transfer tax is charged at a rate of 2% on residential properties and 6% on non-residential properties. In the case of non-residential properties, such as commercial buildings and business premises, this tax was due to rise to 7% from 1 January 2021. This change will not come into effect.

Instead, the general rate will be increased to 8% from 2021. This rate applies to purchases of non-residential properties, such as commercial premises, as well as to purchases of residential properties that are not used as a main residence, e.g. houses that are rented out and holiday homes.

From 1 January 2021 the purchase of residential properties by non-natural persons (e.g. companies, housing associations, etc.) will therefore always be subject to transfer tax at a rate of 8%.

Tip:

Do you want to invest in property and would you like to take advantage of the lower rate of transfer tax while this still applies? If so, the property must have been transferred to you by 31 December 2020!

From 2021 a job-related investment tax credit (BIK) will make it more attractive for companies to make investments. If companies invest in operating assets, they will be allowed to deduct a percentage of these investments from the payroll tax/national insurance contributions they have to pay. Further details will be announced by the government at a later date.

Do you expect your company to post a loss for 2020? And did you make a profit in 2019? If so, it is possible to include a tax reserve in your 2019 corporation tax return. You will then already be able to offset your expected loss for 2020 with your 2019 profit and will therefore pay less tax. However, this is subject to the condition that your loss for 2020 is linked to the consequences of the coronavirus crisis, for example because you had to close your business but still had fixed costs to pay.

The coronavirus tax reserve has been capped at the level of your profit for 2019 without taking this reserve into account. It is compulsory to release the coronavirus reserve in 2020. This measure, which was previously part of a policy decision, is now being included in a legislative proposal.

Please note:

The coronavirus tax reserve is only available to companies that are subject to corporation tax.

In June the legislative proposal on ‘Excessive Loans’ was submitted. Under this proposal debts of a director/major shareholder (dga) that exceed € 500,000 will be taxed from 31 December 2023.

If on 31 December 2023 a dga, together with his/her partner, has a debt to a company in which the dga(indirectly) holds at least 5% of the shares, the excess amount above € 500,000 will be taxed as fictitious regular income in box 2. It will be taxed at a rate of 26.9%. Debts of children, grandchildren, parents and grandparents will also be taxed if they have a debt exceeding € 500,000. This will apply per family member.

Home acquisition debts for which a mortgage right has been granted to the company or that were entered into before 1 January 2023 will not be taken into account.

Example

On 31 December a dga has a debt of € 1,000,000 to his company. € 250,000 of this concerns a debt for the purchase of his own home and was entered into before 1 January 2023. The amount of loans to be taken into account for purposes of the excessive loans calculation is therefore € 750,000. The dga therefore has to pay 26.9% tax on € 250,000 (€ 750,000 -/- € 500,000): € 67,250.

If a dividend is distributed at a later date, this is first offset against the fictitious regular income. This therefore ensures that double taxation is avoided.

Tip:

In 2020 the rate in box 2 is still 26.25%. It may be advantageous to reduce your debts in 2020 by means of a dividend payment.

Tip:

Have you entered into a large amount of debt for property that forms part of your private assets? If so, it may be advantageous to transfer this to a company or your children in 2020 at a transfer tax rate of 2% or 6%.

Director International