Matthijs van Dorssen

Director International

+31(0)88 253 3208 | mvandorssen@alfa.nl

![]()

28 september 2020 | Door: Matthijs van Dorssen

The taxable income for electric cars will slowly be raised each year. A reduction for taxable income on solar panel powered cars is announced. Reductions for energy taxes and a CO2 levy for the industry have been announced.

Last year it was already announced that the addition to taxable income for the private use of electric cars would be increased incrementally. With effect from 1 January 2021 the addition to taxable income for the private use of electric cars will be 12% (2020: 8%) on a maximum value of € 40,000 (2020: € 45,000). Is the list price of the vehicle more than € 40,000? In that case the normal addition of 22% will apply on the amount above this figure.

Example

If a Tesla Model X with a list price of € 110,000 is first registered in 2020, the gross monthly addition will be € 1,492. If this car is not registered until 2021, the gross monthly addition on the same car will be € 1,683.

Over the coming years the addition will be increased further, rising to 16% in 2022 and 17% in 2025. The maximum list price up to which the lower addition is applicable will not be raised and will remain at € 40,000.

One new regulation being introduced this year is that the maximum price will not apply to solar cars powered by integrated solar panels. The government’s intention here is to anticipate developments on the automotive market.

The addition percentage will be fixed for a five-year period, from the first day of the month following that in which the vehicle first enters use.

Tip:

Do you intend to purchase an electric car? If so, make sure it is first registered in 2020. In that way you will make sure you benefit from the lower addition for private use of the car for five years.

The main taxable event for purposes of private vehicle and motorcycle tax (bpm) is currently the time when a motor vehicle is entered in the vehicle licence plate register. This covers both the entry of a motor vehicle in this register and its registration in the owner’s name.

The general rule at present is that the private vehicle and motorcycle tax return must be filed and the payment made before the motor vehicle is entered in the vehicle licence plate register. However, the condition of the motor vehicle at the time of registration determines the level of tax payable.

To simplify the levying of this tax, in future the government wants the taxable event to relate to a single moment in time: the time when the motor vehicle is entered in the vehicle licence plate register.

This proposal should also result in the domestic trade and import trade being treated equally for tax purposes.

The CO2 thresholds for private vehicle and motorcycle tax are being lowered by 4.2%. The rates, i.e. the tax payable per g/km of CO2 emissions (excluding the flat-rate charge), will first be indexed and then increased by 4.38%. In 2021 a stricter CO2 threshold of 77 g/km (2020: 80 g/km) will be introduced for the diesel surcharge. Above this threshold of 77 g/km the rate of the diesel surcharge will rise from € 78.82 to € 83.59 per gram of CO2 emissions.

By taking these measures, the government is aiming to bring the tax base into line with the latest technological developments, which are resulting in ever more efficient and ‘greener’ vehicles.

At present, in the area of energy tax a reduced rate applies to electricity supplied via public charging points. In the case of electricity supplied to a charging point for electric vehicles that have an independent connection, the renewable energy and climate transition surcharge (ODE) has been set at zero (Renewable Energy and Climate Transition Surcharge Act). These two tax facilities were due to be withdrawn at the end of 2020, but have been extended to the end of 2022. With this measure the government’s aim is to stimulate growth of the national charging point network.

The government is proposing to introduce a CO2 levy with effect from 2021. This will apply to large industrial companies that fall under the European emissions trading system (EU ETS) and to waste incineration plants and companies that emit large quantities of nitrous oxide. If these companies’ CO2 emissions exceed the exempted amount set for purposes of the levy, they will pay tax on the portion above this threshold. The levy will be increased up to 2030 and the exempted amount will decrease at the same time. In this way the government hopes to encourage companies to make their production more CO2-efficient.

A number of specific sectors, including horticulture, will be exempt from the CO2 levy. Alternative agreements will be made with these sectors, the details of which are yet to be announced.

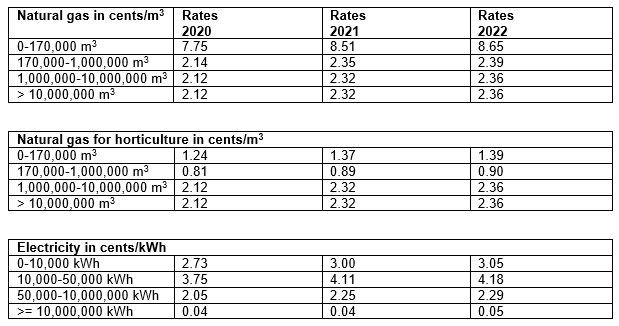

Via the renewable energy and climate transition surcharge (ODE) both households and companies contribute to investments in renewable energy through their energy bill. The ODE serves as the source of funding for spending under the Renewable Energy Transition Incentive Scheme (SDE). In 2021 and 2022 the rates set for the ODE will increase.

The new rates are presented in the table below.

Taxes on energy consist of the ODE and energy tax. In 2021 the tax portion of an energy bill is not expected to increase for a household with average consumption.

Director International