Matthijs van Dorssen

Director International

+31(0)88 253 3208 | mvandorssen@alfa.nl

![]()

19 oktober 2021 | Door: Matthijs van Dorssen

What important tax proposals for entrepreneurs did the caretaker Minister of Finance pull from his briefcase on Prince’s Day? An explanation of the ten most important ones is provided below.

From January 1st 2022 you can grant your employees an untaxed homeworking allowance of up to € 2 per day. This amount is based on a calculation by Nibud (National Institute for Family Finance Information) of the average additional costs incurred, e.g. for coffee and heating, for each day worked at home. Under certain conditions it was already possible to grant an untaxed allowance for setting up a home workstation. An untaxed travel allowance of up to € 0.19 per kilometre for commuting also remains in place for days when the employee travels to the office.

Please note! The travel allowance of € 0.19 may not be awarded to employees on days when they are working from home. That means that if you pay a homeworking and travel allowance, you must always determine the allowance on a per-day basis. You can also opt to follow a practical scheme that has been approved by the legislator.

Read more about the measures for employers.

Paying employees in the form of share options is becoming more attractive. This will allow start-ups and scale-ups to attract talent more easily, for example, and boost new business development in the Netherlands.

At present, tax is paid on share options when the option right received is converted into shares. The downside of levying tax at this moment is that employees (and the employer) pay tax immediately, even though they are not always able to sell the shares yet or do not always have sufficient funds to pay the tax.

From January 1st 2022 employees can decide for themselves when the tax is levied:

Read more about the measures for employers.

In 2022 it will remain possible for directors/major shareholders (DGAs) of innovative start-ups to apply a reduction to their customary salary. This will help to improve the liquidity position of these DGAs. Originally, this scheme was due to expire on January 1st 2022, but this end date has been pushed back one year.

Read more about the measures for entrepreneurs.

For a number of years now the government has been encouraging companies to invest in innovative, environmentally friendly assets by means of the environmental investment deduction (MIA). The MIA allows companies to deduct a percentage of the investment costs from their taxable profit. That means they pay less income or corporation tax.

From January 1st 2022 the percentages are being increased, entitling companies to a higher deduction. Making environmentally friendly investments is therefore becoming more attractive. Three percentages currently apply to the MIA: 13.5%, 27% and 36%. From January 1st 2022 these will be raised to 27%, 36% and 45%.

Which percentage applies to an environmentally friendly asset is indicated on the Environmental List (Milieulijst). The Netherlands Enterprise Agency (RVO) updates the Environmental List at the end of each year. In combination with the Vamil (arbitrary depreciation of environmental investments) scheme your net tax benefit can rise to over 14% of the investment amount.

Tip! Consider postponing your environmentally friendly investments until 2022! Please note that the Environmental List will change from 2022. There is a risk that specific investments will no longer qualify for the MIA from 2022 on.

Read more about the measures for mobility and climate

The government wants to continue to encourage the purchase of zero-emission cars, even though this is costing it more than expected. It is therefore making the following proposal:

Tip! Are you considering buying a zero-emission company car that you will also use for private? Look to get a car that is on a 2021 license plate. The rate of 12% for the extra taxable income over € 40,000 will be applicable for 60 months.

Read more about the measures for mobility and climate

The tax plans include two proposals relating to the income-dependent combination tax credit (IACK):

Read more about the measures for individuals.

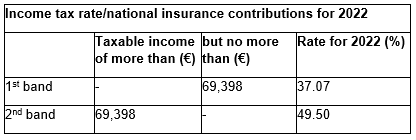

Income tax rates will remain the same as proposed in last year’s tax plan. They will therefore be as follows in 2022:

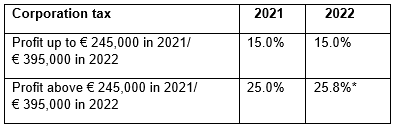

The corporation tax rate for 2022 will also remain as previously announced:

* Preliminary

* Preliminary

Read more about changes in tax rates and taxcredits.

In a judgment the EU Court of Justice has ruled that domestic and foreign companies must be treated equally. In the Netherlands too, domestic companies are treated differently from foreign companies when it comes to refunding forms of advance corporation tax, such as dividend tax. To bring Dutch legislation into line with EU law, the government is proposing the following:

Three changes are being made to the homeownership scheme with effect from 1 January 2022. The scheme is being made fairer by removing unintended restrictions on mortgage interest relief.

To eliminate these restrictions, changes are therefore being made in relation to the home equity reserve, the repayment balance and the existing home acquisition debt (this is a loan taken out to purchase your own home before 1 January 2013).

Read more about the measures for individuals.

Since 1 January 2021 first-time buyers under the age of 35 have not paid any transfer tax when purchasing their home (one-off exemption). Buyers aged 35 and over who will be living in the property themselves have paid 2%, while buyers who will not be residing in the property themselves have paid 8%. Under the government’s proposal, buyers will not automatically be subject to the general rate (8%) if unforeseen circumstances arise after the purchase, but before the transfer. Certain conditions must be met, however.

Read more about the measures for individuals.

Director International

Read about the measurements for different subjects: